Ted Cruz Presents: Bride Of The Son Of The Obamacare Repeal From Hell

He's Baaaaaaack

Senate Republicans have released their second version of a bill to repeal and "replace" the Affordable Care Act, and like the first one, it rolls back the ACA's Medicaid expansion and slashes what's left of the Medicaid program, turning it into a block grant and capping enrollment by state population regardless of how many people need it. The big difference in the new version is that it incorporates that wonderful plan from Ted Cruz (and Mike Lee) that promises to make healthcare plans on the individual market -- the thing most people think of as "Obamacare" -- far worse. In essence, it would create two individual markets: One for younger, healthier people who want to buy cheap "junk insurance" that doesn't cost much, but also doesn't cover much, and another for sicker, older customers who actually need health insurance.

Let's tour the worst of this monstrosity with some guidance from the invaluable Sarah Kliff at Vox, and this excellent Twitter thread from Pennsylvania Senator Bob Casey. The basic shape of the bill -- still going by the name "The Better Care Resolution Act of 2017," which we read with increasingly dark irony -- is much the same. It would still repeal most of the taxes in the ACA, but would keep -- for a time -- two taxes on the wealthiest Americans, to help cover the most expensive patients. Here's the summary from Kliff:

Healthier and higher-income Americans would benefit from the changes in the new Republican plan, while low-income and sick Americans would be disadvantaged. It would create a two-track system for health coverage on the individual market. One would offer cheaper, deregulated health plans, which healthy people would likely flock to. The other would include comprehensive plans governed by Obamacare’s regulations, which would cost more and mostly be used by less healthy people and those with preexisting conditions — a system experts expect would function like a poorly funded high-risk pool.

Deductibles would almost certainly rise under the Republican plan, as would overall costs for low- and middle-income Americans. Individual market participants would have more options to purchase catastrophic coverage, an option likely to appeal to those with few health care costs.

[wonkbar]<a href="https: //wonkette.substack.com/p/senates-obamacare-repeal-will-give-22-million-more-americans-opportunity-to-explore-faith-healing"></a>[/wonkbar]Kliff notes (hah! Bet she never hears that!) that some experts are already saying the new version is unlikely to change the Congressional Budget Office estimate that 22 million more Americans would be left without coverage.

The Cruz-Lee plan would allow insurers to deny coverage to people with preexisting conditions, and also to not cover the "essential health benefits" required under the ACA, as long as each insurance company offers at least one plan that meets all the current Obamacare requirements. Cruz calls it the "Consumer Freedom Act," because people with preexisting conditions would be free to pay through the nose for insurance that actually covers them (or be priced out of the market altogether) while people who are temporarily young and healthy would be free to purchase a no-frills junk insurance plan that might not really cover them if they get sick or have an accident.

Health policy experts know exactly how this would play out: Healthy people would pick the skimpier plan, while the comprehensive plan would essentially become a high-risk pool for sicker Americans.

Individual market enrollees would likely game the system too. A couple expecting a baby, for example, would be expected to upgrade to the plan that covers maternity care for one year before returning to the cheaper plan they had before.

"Someone with chronic illness, they're going to end up wanting to buy the more comprehensive coverage," says Joe Antos, a health policy expert with the conservative American Enterprise Institute. "This means that people with those kinds of illnesses will end up paying more. Even if they receive a federal subsidy, they will likely see higher cost sharing."

Even before the new draft was released, the insurance industry was condemning the Cruz-Lee plan as a recipe for market collapse, making insurance for people who really need health insurance unaffordable and driving up premiums and deductibles across the board. The insurance lobbying group America’s Health Insurance Plans warned:

Unfortunately, this proposal would fracture and segment insurance markets into separate risk pools and create an un-level playing field that would lead to widespread adverse selection and unstable health insurance markets

And that's just the market implications, leaving aside the simple fact that punishing people for being old and sick is evil.

Vox's Ezra Klein puts it a bit more bluntly:

What will happen here is clear: the plans that have to offer decent coverage to anyone who wants it, no matter their healthcare history, will become a magnet for the old and the sick or the soon-to-be-sick, as they can’t afford, or perhaps can’t even buy, the other plans. That will drive premiums in those plans up, pulling younger, healthier people into the non-compliant plans.

The Senate bill thinks it has a fix: a roughly $200 billion fund to offset the costs of sick enrollees. So, in short, what the GOP bill attempts to do is to rebrand high-risk pools as Obamacare plans and make them subsidized dumping grounds for the sick and the old, while everyone else buys insurance in a basically unregulated market.

The new Senate plan would also muck around with who qualifies for subsidized insurance -- where Obamacare offers income-based premium subsidies to anyone on the individual market, CruzCare would limit the tax credits that subsidize premiums to the full-coverage plans. Those buying the cheaper, crappier deregulated plans would not be subsidized. So, hey, the old sick folks would be in OK shape, huh? Not so much, since the costs for full-coverage plans will balloon and the subsidies won't keep pace:

But even after that financial help, these people would still face significant out-of-pocket costs, including high deductibles and premiums. The Congressional Budget Office estimates, for example, that a 64-year-old individual earning $11,500 and receiving tax credits would still need to pay $4,800 to purchase that plan.

Better Hope You Can Move To Canada Care II would, however, allow people to use tax credits to purchase catastrophic-care-only plans, which have huge deductibles but might cover severe illnesses. Such plans were eliminated by the ACA, which sought to provide real insurance to a wider population. With the tax subsidies encouraging these low-premium, high-deductible plans, the insurance market for younger buyers would shift to skimpy, high self-pay plans as the norm.

[wonkbar]<a href="https: //wonkette.substack.com/p/this-goddamned-republican-obamacare-repeal-will-kill-people-time-to-get-into-the-streets"></a>[/wonkbar]Beyond changes aimed at giving an advantage to young, healthy people who will never become old or get sick or have an accident, the revised Senate bill is still every bit as terrible as the first version when it comes to slashing Medicaid, which means people will die, and people with severe disabilities will lose their independence. Considering that the first version's Medicaid cuts were the reason several GOP "moderates" said they would vote "no," we don't see how this new version -- which makes the private insurance market even worse than either the House bill or the first Senate bill -- is going to get any more support, even though this version does add $45 billion to pay for opioid treatment. Considering that Medicaid is among the biggest funding sources for treatment programs, adding a bit of funding while decimating Medicaid isn't likely to win any new friends.

That's where we can at least have some very, very cautious optimism. This puddle of dog's vomit doesn't appear to have the votes needed to pass the Senate, at least not yet. Ted Cruz and Mike Lee (and maybe Jeff Flake) are the only senators who have switched to supporting it, while Rand Paul has already said he's a "no." Susan Collins of Maine also came out against the new bill, so there are the two votes the Rs can afford to lose.* Several R senators say they'll wait to decide until the CBO score comes out early next week. Senate leadership has asked for two scores: one with the Cruz-Lee amendment, and one without, so we'll see whether anyone's swayed. We can't see Dean Heller or Lisa Murkowski signing on to this mess one way or the other.

Also, in a fun attempt to undercut the CBO, some Republicans want to ask the Department of Health and Human Services to score the bill separately, which might be available sooner, but might not mean anything, since the Senate's reconciliation rules require a CBO score. An aide floating that idea claimed the rules only require a "score," and maybe that doesn't have to come from the CBO, but that sounds more like an attempt to win spin points than anything else.

But hell, this is the McConnell Senate -- there's no reason to think these bastards will do anything conventionally.

Shorter version: This is the worst ACA repeal bill yet. It's going to kill people, and make insurance unaffordable for many more. CALL YOUR SENATORS, KIDS.

Update/Correction: We originally said that Rand Paul, Susan Collins, and Ohio's Rob Portman had all said they'd vote no on the new version of the bill. Only Paul and Collins have actually announced they're voting no; Portman is still officially undecided. Wonkette regrets the error.

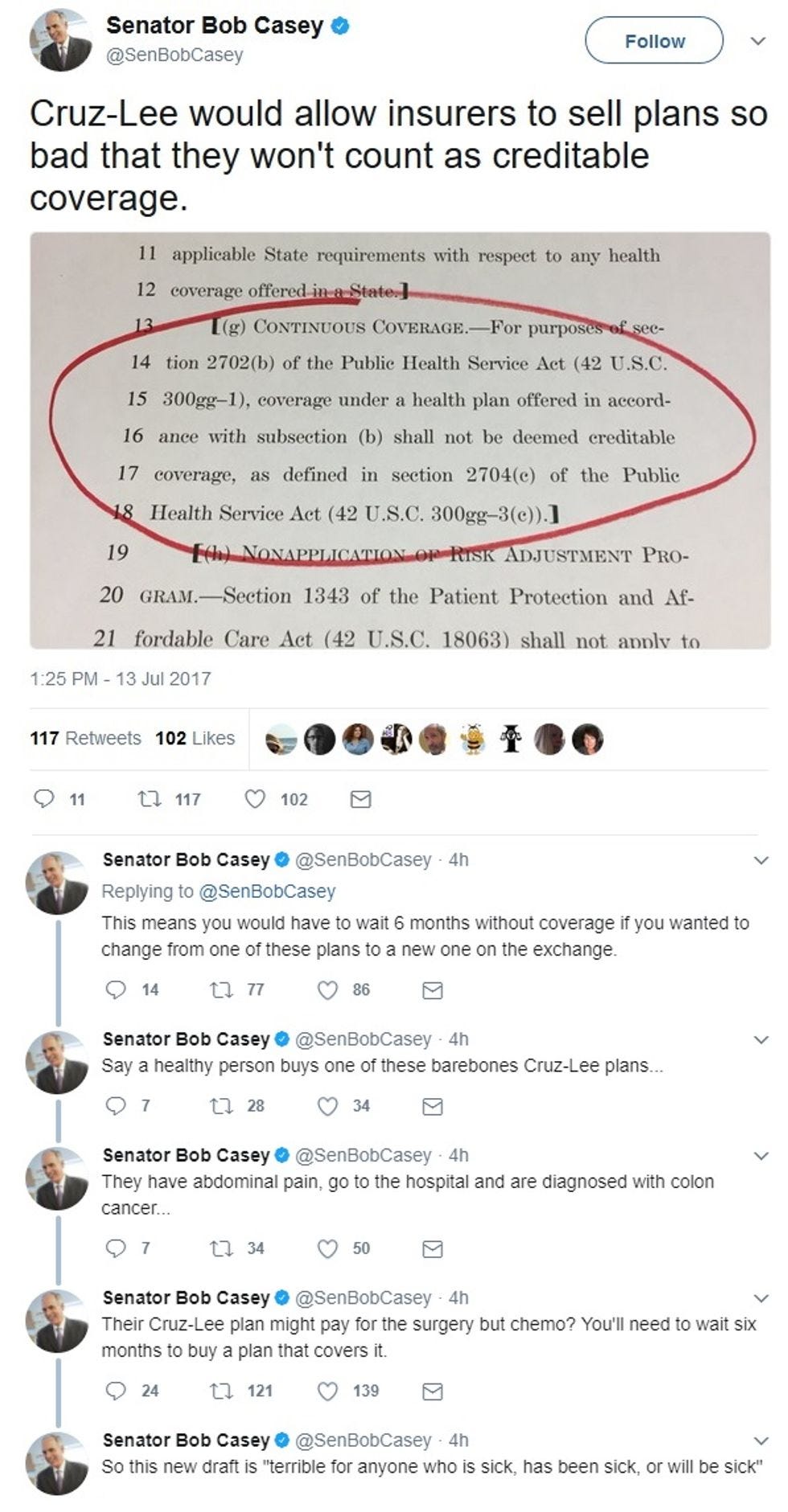

UPDATE: A point from Bob Casey'stwitter thread that also needs to be emphasized: People buying the unregulated plans will be considered "uninsured" as far as the standard of maintaining actual insurance coverage is concerned:

Yr Wonkette is supported by reader donations. Please click the "Donate" clicky to help us keep bringing you the horror show.

[ BRCA Draft from Senate Budget Committee / Vox / WaPo / Politico / Vox / Politico ]

I hear they chose a very nice font for it, though.

right but then apparently - even tho you've satisfied the mandate - you can still be locked out of ACA compliant plans (e.g., the good stuff) for 6 months because...wait for it: you bought cheap crap.

soviet nesting doll of insurance. ouroboros of insurance.